Why Chargebacks Happen and Early Response

Posted on Feb 26, 2026Aengus Neary | 7 minute read

What is a Chargeback and Why It Happens

Where Chargebacks Sit in the Merchant Process

A chargeback is not just a refund processed by the bank. It is a formal card scheme process that reverses revenue, imposes strict response deadlines, and influences fraud and dispute monitoring metrics.

For merchants, a chargeback represents both financial impact and decision responsibility. The key stages as well as the points at which exposure and control shift are outlined below.

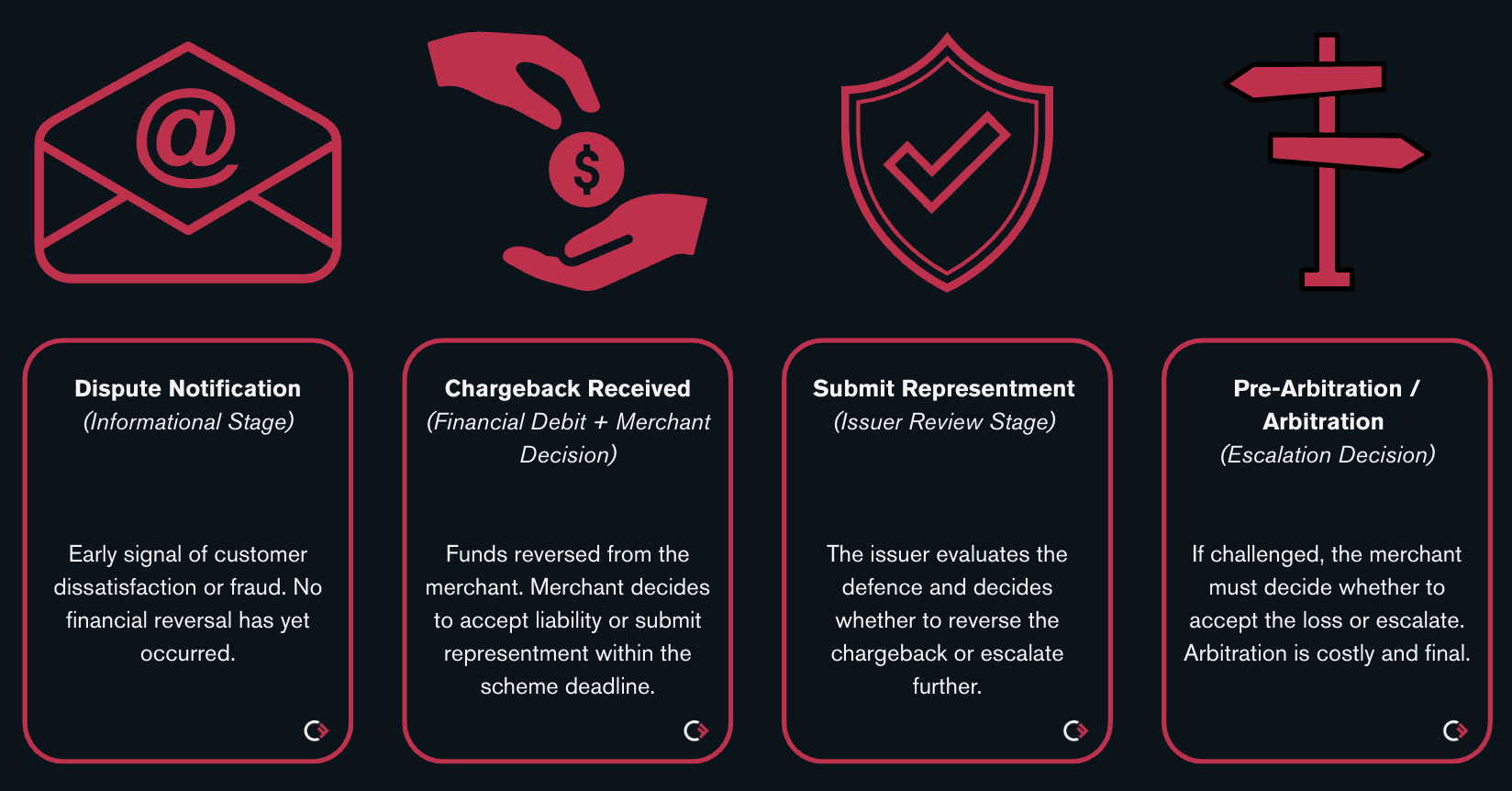

Simplified Merchant-Facing Lifecycle

This view is simplified to focus on direct financially relevant stages.

Why is a chargeback raised?

Chargebacks are raised when a cardholder disputes a transaction with their issuing bank. Historically, this mechanism was designed to protect consumers in cases of genuine error or fraud. Today, disputes arise for a broader range of reasons, including convenience and customer behaviour patterns.

Common reasons a chargeback is raised include:

- The cardholder does not recognise the transaction

- Goods or services were not received as expected

- A refund was expected but not processed

- The transaction was genuinely fraudulent

- The chargeback route is perceived as faster than contacting the merchant

Importantly, not all chargebacks indicate malicious intent. Many are driven by confusion, poor post-purchase communication, unclear billing descriptors, subscription misunderstandings, or friction in cancellation flows.

For merchants, this distinction matters. Some disputes reflect fraud risk, while others reflect customer experience gaps. Effective chargeback management therefore requires understanding not just how to defend disputes, but why they are occurring in the first place.

Fraud and Non-Fraud Chargebacks

From a risk and operational perspective, chargebacks are typically grouped into two broad categories: Fraud and Non-Fraud. The distinction is important because the financial, monitoring, and prevention implications differ materially.

Non-Fraud Chargebacks:

Often referred to as service or dispute chargebacks, these are driven by experience-related issues such as:

- Confusing billing descriptors

- Poor checkout or post-purchase communication

- Delayed shipping or unclear delivery expectations

- Friction in refund or cancellation flows

- Additional/Unexpected charges post-purchase

- Product/Service dissatisfaction

Many non-fraud chargebacks are, in practice, customer journey failures. Improving transparency, communication and refund handling often reduce these disputes more effectively than additional fraud controls.

It is also increasingly common for non-fraud reason codes to be used in cases that resemble 1st Party misuse, blurring the line between service issues and opportunistic behaviour.

Fraud Chargebacks:

Fraud chargebacks carry higher risk for merchants because they affect fraud ratios and scheme monitoring programs, while non-fraud chargebacks can impact dispute monitoring programs as well as VAMP (Visa Acquirer Monitoring Program).

These are raised when a cardholder claims they did not authorise the transaction. Fraud chargebacks can be largely split into 2 segments: 3rd Party Fraud and 1st Party Fraud:

3rd Party (aka “Malicious Fraud”)

When stolen card details are used by an unauthorised party. Historically, this represented the majority of fraud chargebacks.

Since the cardholder has no relationship with the purchaser, little to no evidence can be used to defend these chargebacks. As a result, many merchants treat confirmed third-party fraud chargebacks as operational write-offs, focusing their resources on prevention rather than defence.

1st Party Misuse (aka “Friendly Fraud”)

When the cardholder themselves initiated the purchase and later disputed the transaction, claiming to the bank that it wasn’t them. In recent years, this has increased substantially, driven in part, by changes in consumer behaviour, subscription modelling, shared cards within households, buyers remorse and increased awareness of dispute processes.

Unlike Malicious Fraud, Friendly fraud cannot be prevented solely through stricter controls at checkout. This is because a ‘Friendly Fraudster’ looks like a genuine customer until the fraud dispute is initiated.

Instead, Merchants will aim to mitigate through clear policies, strong transaction history and effective defence strategies.

When does the Merchant feel the impact of a Chargeback

A merchant feels the impact when a dispute converts into a formal chargeback. At this point, the transaction is reversed (returned to the cardholder), chargeback fees are applied, internal handling costs are incurred and monitoring ratios are affected.

For a more detailed breakdown of cost impact when a chargeback is created, refer to this previous article.

In practice, the merchant can take the following steps avoid a dispute becoming a chargeback:

- Enhancing Prevention controls at checkout to prevent malicious fraudulent payments from being authorised.

- Improving customer journey through checkout to give the consumer clarity about their purchase.

- Implementing Avoidance solutions that address disputes when raised, before they turn into a chargeback.

These methods can be effective when well executed, but some chargebacks will still be received. The objective is therefore not elimination, but disciplined coordination across prevention, avoidance and defence.

Chargeback Intake and Decisioning

When a chargeback is received, the objective is to move quickly but with control. The first stage is not building a defence; it is protecting revenue, enforcing the deadline to defend (typically between 30-45 days but varies depending on scheme/reason code) and determining whether defence is commercially rational.

Immediate Control

A chargeback should be logged and flagged as soon as it is received. Because the issuer has already provisionally credited the cardholder, issuing a separate merchant-side refund results in avoidable double loss. The order should therefore be marked to prevent duplicate reimbursement, provide a fraud label for enhancing prevention controls and to alert customer service teams in case of related contact from the customer.

The response deadline must also be recorded at intake. Chargeback timeframes are scheme-defined and limited. Missing the submission window removes the right to defend. Clear internal SLA’s and assigned ownership reduce expiry risk and create accountability.

Categorisation and Assessment

Once controlled operationally, the chargeback should be categorised by reason code and dispute type. This determines both the evidentiary standard and the likelihood of success.

At this stage, the merchant is assessing defendability rather than preparing documentation. Key questions include:

- Is there strong authentication or authorisation data?

- Is there proof of delivery or service usage?

- Does customer history suggest first-party misuse?

- Is there evidence of prior communication or refund denial?

Equally important is validating whether the dispute reflects a merchant-side issue, such as duplicate charging, fulfilment failure, or unclear policy communication. Where an internal fault exists, acceptance is often more economically rational than defence.

Accept or Defend

The decision to represent should be deliberate. Not all chargebacks warrant defence.

Merchants should consider dispute value, estimated win probability, operational cost, and potential escalation risk. Low-value disputes with weak evidence may not justify resource allocation. Higher-value disputes with strong evidentiary position typically do.

This decision point is strategically important. Win rates alone are not meaningful without understanding which cases were intentionally accepted.

In addition to this, a won defence can recoup the disputed amount but does not reverse the hit on a merchant’s fraud ratio.

Scaling the Process

As dispute volumes increase, manual chargeback review becomes inconsistent and resource-intensive. Advanced merchants introduce rules-based decisioning or automation to standardise accept/defend logic to improve scalability.

Automation should enhance consistency, but not replace oversight. Clear governance and monitoring remain essential to avoid systematic misclassification while scaling.

Conclusion

Chargebacks are rarely isolated events. They are signals of fraud exposure, customer friction, or internal process breakdown. Understanding why they occur and responding with control at the point of intake determines whether they become contained losses or recurring structural weaknesses.

Early discipline matters. Clear ownership, structured assessment, and deliberate accept-or-defend decisions protect recoverable revenue and prevent avoidable escalation or operational costs. Without that control, even strong prevention and customer experience improvements will fail to translate into measurable impact.

For merchants seeking to bring greater structure and consistency to this early-stage handling, Chargeforwards supports that progression, enabling smarter ML decisioning, stronger governance, and more controlled chargeback management from the moment a dispute is received.